I have often been in conversations with entrepreneurs who confuse Profit Margin with Return on Investment when evaluating the financial feasibility of a business. Although sometimes this confusion is caused by simple ignorance, in many others it is motivated by an attitude rather simplistic. Bill Gates himself, while being interviewed about the beginnings of Microsoft by Walt Mossberg and Kara Swicher on the All Things Digital D6 conference, responded to Kara’s question as follows:

Kara Swicher: Bill, “Do you consider yourself a businessman or do you consider yourself more of a technologist?”

Bill Gates responds humorously and sarcastically: “Sure! You know! Sales minus costs equals profit”.

Everyone laughed for a moment and then Bill continued to ask still in a humorous and sarcastic way: “Is there anything more than that?” Everyone broke out in laughter again. I also remember a conversation I had with a young Dominican businessman in which he expressed the following: “Based on my experience, I can tell you that to be successful in business you only requires three things: sell at a good price, spend little and collect receivables.”

So what is Profit Margin and what is Return on Investment?

Profit Margin is a measure of the proportion of earnings you can get out of every dollar ($) of revenue. In other words, if we think of a business that generates US$ 2,000,000 a year in revenue, and to generate such revenue incurs in costs of US$ 1,800,000 the remaining US$ 200,000 is the profit, and we can say that the business has a profit margin of 10% (US$ 200,000 / US$ 2,000,000).

Return on Investment measures how much profit is generated by every dollar ($) invested by the shareholders in the business. So, if the shareholders of the above-mentioned business invested US$ 1,000,000 in it, then we can say that the shareholder’s Return on Investment is 20% per year (US$ 200,000 / US$ 1,000,000).

In short, Profit Margin measures the level of profits in relation to revenue, while Return on Investment measures the level of profits in relation to the amount of money invested in the business.

Return on Investment is calculated at specific periods or frequency

Unlike Profit Margin, when we talk about Return on Investment we always include the time factor. In other words, Return on Investment is calculated for a specific frequency, typically annually and sometimes monthly. In the graphic above, because our computations were based on revenues, costs and profits of a year, the return we got was expressed on an annual basis. However, for each annual return, there is an equivalent monthly return which is approximately 12 times smaller. Let’s review again the graphic above. If we prorate the annual earnings, we get monthly earnings of US$ 16,667, and then we can compute a monthly Return on Investment of 1.67% per month (US$ 16,667 / US$ 1,000,000). Therefore, one can say that this business generates an annual return of 20%, which equals to a monthly return of 1.67%, and has a Profit Margin of 10%.

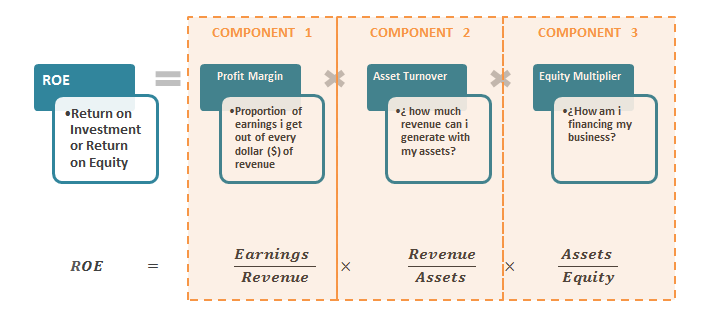

The relationship between Profit Margin and Return on Investment

What is the relationship between Profit Margin and Return on Investment? What other factors affect Return on Investment? The most straight-forward way to answer these questions is by looking at the DuPont Equation. This equation was created by an engineer who performed as executive of the treasury department of the DuPont Company in 1914. This simple equation helps us identify three basic components that together define Return on Investment: the Profit Margin, the Asset Turnover and the Equity Multiplier.

If we apply the DuPont Equation to the business illustrated above, we have that the profit margin is 10% (Profit of US$ 200,000 / Revenue of RD $ 2,000,000), the Asset Turnover is 2 (Revenue of US$ 2,000,000 / Assets of US$ 1,000,000), and the Equity Multiplier is 1 (Assets of US$ 1,000,000 / Shareholders’ Equity of US$ 1,000,000), therefore, through the DuPont Equation we confirm that the Return on Investment of this business is ROE = 10% X 2 X 1 = 20% per year.

Also, the DuPont Equation shows us how Profit Margin is actually one of the main components of Return on Investment. In fact, as long as the other components are unchanged, we can say that the greater Profit Margins will yield greater Returns on Investment. Now, how do Asset Turnover and Equity Multiplier affect the Return on Investment?

Asset Turnover is related to the efficiency with which we use the assets or means of production of our business; i.e., machinery, equipment, inventory, working capital, among others. In other words, this variable measures the amount of revenue that we generate in relation to the assets that we have. For example, if we assume that the business illustrated above is able to increase its annual revenue to US$ 3,000,000 without making additional investments while maintaining its Profit Margin in 10%, then the asset turnover increases to 3 (Revenue of US$ 3,000,000 / Assets of US$ 1,000,000) and with the DuPont Equation we can compute that the Return on Investment is now ROE = 10% X 3 X 1 = 30% per year.

The Equity Multiplier reflects how we are funding the business. When installing a business we have the option to use only our own capital or to finance part of it by a loan. This is what is commonly called financial leverage. Through the DuPont Equation one can identify two direct effects of Leverage on Return on Investment: 1 -) Because the loan allows us to acquire the same amount of assets with a smaller investment from shareholders, the Equity Multiplier increases and positively affects the Return on Investment 2 -) But at the same time, because the loan pays interest, the profit margin decreases and negatively affects the Return on Investment. In economies with efficient financial markets and stable interest rates, the net result of these two effects is usually positive, therefore, leverage tends to positively affect Return on Investment for shareholders. If we return once again to the business illustrated above and assume that the shareholders decided to finance half of the purchase of assets (RD $ 500,000) through a bank loan that pays an interest rate of 16%, then we have the following: the Profit Margin will be reduced to 6% (profit after subtracting interest of US$ 120,000 / Revenue of US$ 2,000,000), the Asset Turnover remains in 2 (Revenue of US$ 2,000,000 / Assets of US$ 1,000,000) and the Equity Multiplier increases to 2 (Assets of US$ 1,000,000 / Shareholders’ Equity of US$ 500,000). Therefore, the DuPont Equation shows us that the Return on Investment for shareholders is now ROE = 6% X 2 X 2 = 24% per year.

As we can see, the DuPont Equation is a very simple and practical tool that allows us to understand very clearly, not only the difference between Profit Margin and Rate of Return and the relationship between these two variables, but also how other key variables affect the Return on Investment. Finally, we hope that these simple ideas will be of practical use for you when making business decisions. After all, now you can say that you know more about Finance than Bill Gates himself!